Supply chains, interconnectedness and pandemics: From global value chains to Covid-19

Advisory Panel Member Paolo Garonna presents this detailed analysis of the macro-economic and financial impact of Covid-19, and possible global scenarios, advising on what action should be taken at global and national levels right now

This Time Is different: Pandemics in the 21st Century

Covid-19 caught the world unprepared: why did it originate in China? Why did it spread so rapidly in Italy and Spain? Why Korea and Iran?

Many basic questions have remained unanswered, structural uncertainty and the streetlight effect (a type of observational bias that occurs when people only search for something where it is easiest to look).

Yet the most relevant questions concern the future: How will the crisis evolve? Will the spread be V-shaped? U-shaped? Or will it be L-shaped? How will it affect the economy? What about financial stability? Will it cause temporary or frictional effects, or structural and permanent ones?

One of the major differences in this outbreak compared to those of the past is that the list of the ten current countries that are most affected is almost identical to that of the world’s ten largest economies. Never has the saying ‘when these economies sneeze, the whole world catches a cold’ been more appropriate.

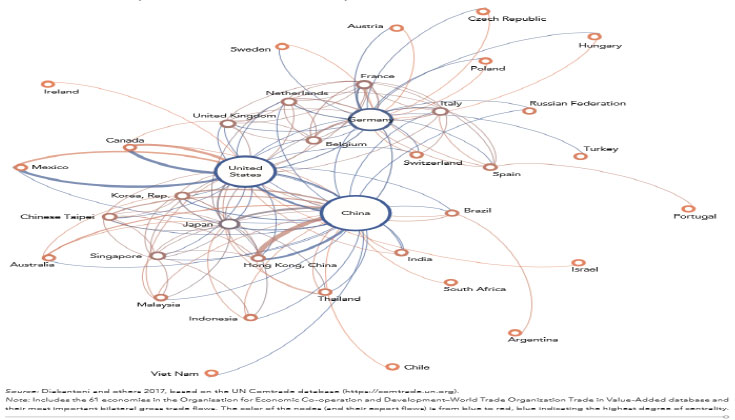

The countries that are most involved are also at the core of global value chain (GVCs, or supply chains – see chart below) interconnectivity, and Covid-19 affects both manufacturing and supply. This manifests not only in bottlenecks and disruptions, but also in services and demand industries, such as tourism, retail, travel, restaurants and so on.

The Epidemiological Response

The first policy measures that were taken appear to have been inconsistent, uncoordinated, often emotional (or driven by political motives), national or local, rather than international and global (as they should be for a global pandemic).

The Covid-19 virus is new and unknown, so no therapies, vaccines or experience are available to draw upon. This has meant that the public health response has – on the whole – been similar to responses centuries ago, ie highly disruptive.

The objective of emergency measures is to flatten the epidemiological curve through social distancing and isolating infected populations via quarantine or hospitalisation. This saves lives directly by reducing the contagion, and indirectly by avoiding the collapse of healthcare systems.

However, containment is very costly in economic, political and social terms, so it is a mitigation measure. Moreover there are complex and delicate trade-offs that have to be managed.

Containment and Mitigation: Compliance, Effectiveness and Trade-Offs

The more radical the containment measures – economic shutdowns, travel bans, shop closures, etc – the greater the social and economic cost, particularly in regard to post-crisis recovery

Another dilemma is that the more effective the containment is in saving lives, reducing contagion and so on, the longer the duration of the emergency, bringing with it even greater social and economic disruption (see graph 1).

Typical cognitive biases imply that in the early stages of contagion, risks are underestimated with governments and public opinion not prepared to take bold measures. In the later stages of the crisis, conversely, risks are overestimated, possibly generating panic and unrest (see figure 2).

Graph 1: Epidemiological curve with and without containment

Graph 2: From underestimation to over estimation

Exponential growth bias is also frequent. Intuitively, we tend to ‘linearise’ exponential functions – another reason why threats are underestimated in the early stages. As contagion does not spread evenly or predictably, and decisions are decentralised, there is generally no co-ordination or synchronisation. Thus even if – and where – containment is successful, relaxation of restrictions cannot be undertaken lightly, for fear of rebound or repeated waves of infection.

The Resilience of Health Systems

An effective health system should be able to adopt mitigation measures in terms of building new hospitals, hiring doctors, transferring patients and exploiting any spare capacity by expanding, relocating and reorganising its resources. However, most public and private systems do not have such flexibility. The former tend to have easier access to state support and last-resort financing in an emergency situation, but are liable to be more rigid and less flexible. Private health systems have greater flexibility, but are constrained by tight private budgets and self-interest.

Ultimately, resilience should be built into the system in advance rather than in the midst of a crisis, based on the right balance between public and private players and responsibilities.

Resilience is linked to the credibility and reputation of institutions and leadership. A recent survey measured public trust in health services and some of the results are telling: Korea 86 per cent, Germany 80 per cent, Italy 63 per cent, and the US 59 per cent. Social capital and trust bring about acceptance of and compliance with bold and hard restrictions such as quarantines and therefore warrant the effectiveness of containment.

Monitoring the Contagion Risk: Data and Measurement Problems

Little is known about Covid-19. Virology research is engaged in understanding how the disease is transmitted, what damage it causes, how to cure it, and the possibility of a vaccine or antibodies testing.

A big problem for monitoring the risk of infection is that data and indicators are few and of poor quality. The main measures are prevalence (how widespread the disease is) and incidence (the number of new cases or the risk of contracting the disease). The two are related through duration (prevalence = incidence x duration).

Incidence is easier to measure, but the problem depends on testing. Testing standards and practises are diverse, inconsistent, uncoordinated and often unreported (see graph 3), so incidence is generally underestimated. This means that the total number of cases is unknown, and the number of confirmed or suspected cases depends critically on the scale of testing.

In order to determine contagion risk, we need to know the prevalence of the virus, but this is very difficult to measure directly. Incidence and duration could be measured in principle, but this requires substantial investment in testing and statistical research.

This is why mass testing is generally considered the most effective monitoring strategy. But it is expensive and time consuming. Countries such as China and Korea, which have taken recourse to mass testing, seem to be more successful in containment.

There should be international norms and standards on testing and reporting, according to the World Health Organisation (WHO). Greater use should be made of randomised controlled experiments or sample surveys. Monitoring should be entrusted to independent technical bodies, free from political interference.

To monitor contagion risk effectively we need more research, more data and better quality data, big data, IOT and more technology.

Graph 3: Reported Number of Tests for Covid-19 as of March 20, 2020 (source: Our World in Data)

Link with GVCs: the Covid-19 Supply Chain Contagion

Mapping Covid-19 contagion risks shows remarkable similarities with a map of global supply chains, supporting the hypothesis that the latter has had a role in the transmission of this virus. In Graph 4, we see trade flows of intermediate inputs in the textile sector and the main interconnected hubs. China appears to be central to the entire global network of trade and production, but there are also strong regional dimensions: Italy is the heart of ‘Factory Europe’, as is the US in North America (see Baldwin and Tomiura 2020).

Graph 4: Mapping GVCs for the textile sector

In Graph 5, we have the same information for ICT. The graph shows also that there are significant sectoral differences (asymmetric shock).

Graph 5: Mapping GVCs for the ICT sector

It is likely that textiles, footwear, machine tools, etc, have higher Covid-19 rates of infection than other sectors, because they involve more interpersonal contacts, more SMEs, and less advanced technology. However, more interdisciplinary research is needed on this.

The relationship also works in the other direction (interconnectedness): the epidemic’s progression will strike GVCs hard and directly, affecting trade and investment in individual countries, regions and the world.

In terms of manufacturing, the three hardest-hit East Asian manufacturing giants (China, Korea, Japan) account for over 25 per cent of US imports, and over 50 per cent of computers and electronics imports

Apparel and footwear sectors are particularly vulnerable to East Asian supply disruptions. They are also the sectors most vulnerable to epidemic contagion.

As GVCs exploit their inbuilt flexibilities by diversifying suppliers, location, customers, production methods and so on, they will also contribute to spreading the virus more widely

More on Economic Disruptions

Vulnerability to disruption is also related to conventional practises to keep lean inventory levels and oligopolistic positions (technological niches) in the provision of components and intermediate products. This is particularly true in electronics and ICT.

The optics sector is highly exposed. Hubei province is China’s ‘optics valley’, where most manufacturing of fibreoptic components is located; these are essential inputs for telecommunications’ networks. Twenty-five per cent of world’s optical fibre cables and devises and highly advanced microchip factories (such as the flash memory chips used in smartphones) are located in Hubei.

The Economist (March 7, 2020) cites conjectures that the Hubei disruptions alone could knock 10 per cent off global shipments of cell phones.

Policy reaction is therefore critical, as Weder di Mauro states: “The size and persistence of the economic damage will depend on how governments handle this sudden close encounter with nature and with fear… Government reactions create more and longer-lasting disruptions than the virus.”

Emergency closures and bans are highly disruptive. Shutting down an economy is not like switching off a light bulb, but is more like shutting down a nuclear reactor, with serious risks of meltdown and financial shocks.

The Macro-Economic and Financial Impact of the Pandemic

We have dealt so far with the direct impact of the virus on GVCs. But the indirect economic effects of the pandemic are even more worrying. They also operate mainly via global supply chains, whose disruption can have a devastating impact on the world economy, both on the demand and the supply sides.

Several economic forecasts have been released (see reading list below) and most commentators agree that the global economic and financial crisis that is unfolding might become worse than the 2008-9 crisis if it not addressed properly and promptly.

Critical factors in this instance are going to be the controls of cognitive distortions and gaps in leadership. Here are a few guidelines:

Public health concerns should take priority, but economic and financial policies require careful consideration too. Managing wisely and authoritatively the many and delicate trade-offs in play requires credible leadership and informed decision-making.

Prudential restrictions, such as lockdowns and quarantines should not be seen as leisure or holiday periods. All available technological and organisational opportunities should be exploited for intensifying work and business efforts, while remaining safe. I refer here to smart or home working, distance learning, virtual meetings, etc.

Solidarity should promote public and private initiatives in favour of the most vulnerable, who are going to be hit more by the virus and its impact in terms of morbidity, casualties, human suffering, poverty and exclusion.

Since pandemics are a global phenomenon, the response should also be globally planned and acted upon with international dialogue and co-ordination. Co-operation in research, technology, policy analysis and the exchange of best practice are required. We have already mentioned the need to establish rules and mechanisms for monitoring risks and to make data comparable (eg standards for testing and reporting). A co-ordinated response from Central Banks on an accommodative monetary policy would also be necessary.

The Way Forward: What Future for GVCs?

Global supply chains have slowed down in the last few years. This may be down to contingent and cyclical factors, the legacy of the past financial crisis, policy restrictions to trade and investment, trade conflicts, etc.

But it could also be due to structural and permanent transformations (‘new normals’): Rising wage costs in emerging economies; geopolitical risks and risk diversification; rising transport and off-shoring costs; and shift in politics and public opinion.

Digitisation, ICT and automation play a large role. These factors are reversing the importance and length of GVCs, reorienting production towards OECD economies (see OECD)

The ongoing pandemic promises to be a game changer. It will likely produce disruption and discontinuity in GVCs. In what direction? It all depends on how effective the policy response to the crisis will be, and correspondingly how long the crisis will last. In 2008, the G20 of most developed nations was given a leadership role, a co-ordinated fiscal stimulus was agreed and Central Banks promoted convergence in monetary policy. Will global leaders be able to do the same now?

Meanwhile, European integration drags on in a climate of mistrust and petty intergovernmental quarrels. The EMU, Banking Union and CMU are still incomplete and vulnerable (see Coeuré). More ambitious projects are stalled.

The evident links between GVC and the Covid-19 contagion might give ammunition to all those who object to globalisation and want to put the brakes on GVCs.

Here are two possible global scenarios:

Scenario 1. Deglobalisation and nationalistic retrenchment: Policy reactions could hinder the flow of goods, service, technology, and especially people. This could well make the economic effects more persistent (see Weder di Mauro). Disruption could also imply sudden deglobalisation. Vulnerability to health shocks will be taken into account by individual decision-making and risk management among companies and banks. Societies might react with xenophobia, closing borders and searching for scapegoats. In times of rising populism, the threat of disintegration and conflict is growing.

Scenario 2. Global governance of value chains and related risks: International co-operation and co-ordination should be strengthened. Real powers and budgets should be given to multilateral agencies such as the WHO, UN, IMF, etc. Cross-country market mechanisms, such as insurance, finance, health sector, research, ICT, etc, should be facilitated. International standards and last resort intervention mechanisms should be developed. In terms of enhancing preparedness, risk reduction and risk sharing, resilience, co-ordinated emergency responses, investment in infrastructures, including human and social capital, solidarity funds for the most vulnerable, economic growth, sustainable development and financial stability, should be considered.

The Conditions for a Successful Post-Emergency Recovery

Rebuilding trust, particularly in science and research. Research on pandemic threats and other global risks is a global public good. But the private sector – from health care to insurance – should also invest in research. We need trust in democracy, freedom and good governance. This requires investment in human capital, ethics, life-long learning, labour management relations, international dialogue and co-operation. We also need responsible use of technologies because trust, like mistrust, can be contagious thanks to the web and social media

Responsible leadership. “Reactions to Covid 19 will be like a Rorschach blot test” of leadership, government and the resilience of our societies, according to Wyplosz. People will realise the importance of democratic accountability and the quality of elected politicians, and vote more responsibly. The failings of healthcare systems will be corrected, and there will be consensus for reforms (however painful they might be), social engagement, global cooperation, openness and solidarity.

A healthy reaction to populism and political extremism. People realise the contradictions of xenophobia and sovereignism: on the one hand, it preaches the closure of borders, protectionism and autocracy. On the other, it demands help from other countries, foreign technologies, life-saving goods and services, the gains of global dialogue and co-operation, including GVCs.

Europe’s global leadership. We need to rebuild global leadership, based on multilateral co-operation, shared values, dialogue, agreed rules and effective global institutions. Europe can provide a decisive contribution to this new world order. It must, however strengthen its governance mechanisms and socio-economic integration.

Sources:

Baldwin and Weder di Mauro, Economics in the Time of Covid-19, a VoxEU ebook, CEPR Press, London, 2020

Wyplosz C, The good thing about coronavirus, in Economics Covid-19, op.cit.

OECD, The Future of Global Value Chains, Business as Usual or a New Normal?, OECD Policy Papers, n.41, Paris, 2017

WTO, Global Value Chains Development Report 2019, Technological Innovation, Supply Chain Trade, and Workers in a Globalised World, Geneva, 2019

Demertzis M, The cost of coronavirus in terms of interrupted global value chains, Bruegel Blogpost, 9-3-2020, Brussels

Garcia-Herrero A, Epidemic tests China’s supply chain dominance, Bruegel Blogpost, 17-2-2020, Brussels

Demertzis M et al, An Effective Economic Response to the Coronavirus in Europe, Bruegel Policy Contribution, n.6, Brussels, 11-3-2020

ECDC, European Centre for Disease Prevention and Control, Outbreak of Covid-19: increased transmission globally – fifth update, Stockholm 2-3-2020

Gaspar V, Fiscal Policies to Protect People During the Coronavirus Outbreak, IMFBlog, IMF, Washington D.C., 5-3-2020

Adrian T, Monetary and Financial Stability During the Coronavirus Outbreak, IMFBlog, IMF, Washington D.C., 11-3-2020

Taglioni D, Winkler D, Making Global Value Chains Work for Development, IBRD/The World Bank, Washington DC, 2016

World Trade Organization, Measuring and Analyzing the Impact of GVCs in Economic Development, Global Value Chain Development Report 2017, The World Bank, IDE-JETRO, OECD, UIBE, WTO, Washington DC, 2017

World Economic Forum, The Shifting Geography of Global Value Chains: Implications for Developing Countries and Trade Policy, WEF, 2012

Elms D, Low P, Global Value Chains in a Changing World, WTO, Fung Global Institute, Temasek Foundation Centre for Trade and Negotiations, WTO Publications, Geneva, 2013

De Backer K, Miroudot S, Mapping Global Value Chains, ECB Working Paper Series, n.1677, Frankfurt, May 2014

OECD, Interconnected Economies: Benefitting from Global Value Chains, Paris, 2013

Ortiz-Ospina E, How many tests for Covid-19 are being performed around the world?, Our World in Data, University of Oxford, 12-3-2020

Roser M et al, Coronavirus Disease (Covid-19), Our World in Data, University of Oxford, 12-3-2020

OECD, Health Statistics, Definitions, Sources and Methods, OECD, Paris 2016

IMF, Potential Impact of the Coronavirus Epidemic: What We Know and What We can Do, IMF Blog, Washington DC, 12-3-2020

Meninno R, As the Coronavirus spreads, can the EU afford to close its borders?, Bruegel Blogpost, Bruegel, Brussels, 12-3-2020

Garcia-Herrero A, Uncoordinated Policies behind market collapse, Bruegel Opinion, Bruegel, Brussels, 12-3-2020

Coeuré B, The single currency: an unfinished agenda, ECB, Frankfurt, 3-12-2019

The Economist, Covid-19: New World Curriculum, Briefing: Covid-19, Issue 7-3-2020, London

Paolo Garonna, 29/11/2020